Building an innovative technology business is very challenging due to the unpredictable nature of science, the capital requirements, but also due to the different hurdles along the commercialisation path, including technology development, prototyping, pilot scale testing, choosing the right pricing and business model, as well as regulatory requirements.

To add to all these challenges, valuing the initial intellectual property (IP), usually involving patents (and/or copyright in software inventions), is very difficult as the future income and market valuing methods require information that does not exist yet, or in the case of the cost methods, they do not account for the potential of the technology. Market comparables also neglect the future income generating potential of the IP portfolio in question.

As challenging as it seems, it is not impossible. Innovative technologies just require a lot more research for the data required as input in the models. The best way to approach this is holistically, by combining all the comparable market data found on the early technology with a future income model and allowing for broader sensitivity analysis of the main parameters. However, it is worth noting that the results are only as good as the data you use for the calculations.

Worked example

The valuation process requires careful consideration of various internal and external factors, regardless of the maturity of the technology area. However, early-stage innovation hotbeds are particularly sensitive to the impact of said considerations and therefore necessitate extra analysis.

The best way to visualise the process and its intricacies is through a worked example. Considering the drawbacks of the market and cost methods being inadequate for early-stage technology valuations, the discounted cashflow method on potential future earnings is the best way forward.

As with most inventions, before any income can be generated, a lot of time and money is required to develop it, so for the first few years, the cashflow is going to be negative. First hurdle in the valuation journey is assessing how much it will cost to develop the technology. In one instance, if the product is not very complex, we can make a development plan and add up the costs (at a premium as there usually is some additional unexpected spending). An alternative would be to analyse companies already in the field and find out how much money they have raised and how long it took them to get their product to market. Investment information is not usually freely available but can be found on platforms such a Pitchbook or CrunchBase.

For the purpose of the example, we will work under the assumption of a £500,000 investment requirement and two years of development. For the ease of calculation, we will assume the cost to be spread equally over the years.

Now that we have our commercial product, we need to understand our potential future revenues, sale quantities, pricing and the year-on-year sales growth. How many products we would sell depends a lot on how many players there are in the field, their market share, and the industry itself. The competitive advantage that we might have over competing products will dictate the price premium that we could charge for the product, whilst the growth rate will be based on what growth rates other early-stage companies have.

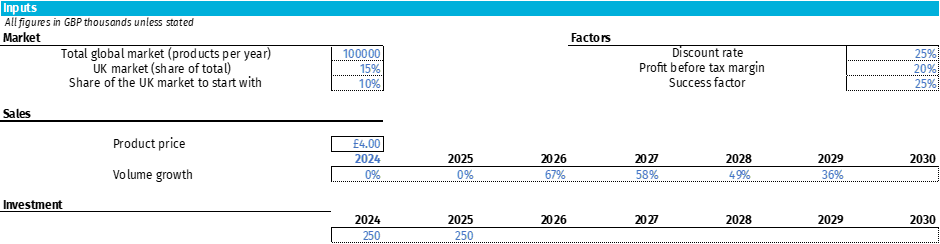

Again, for the purpose of our calculations, we will work under an assumption that our total global addressable market is 100,000 products per year, with 15,000 products per year in the UK alone, but we forecast that we start with a 10% penetration rate and then we expand with certain growth rates (67% in Year 1, 58% in Year 2, 49% in Year 3, 36% in Year 4). A good benchmark to use is to review financial filings of a public company in the same industry and use them as a proxy (as an early-stage business is not likely to have the reputation and established client base to guarantee such rates).

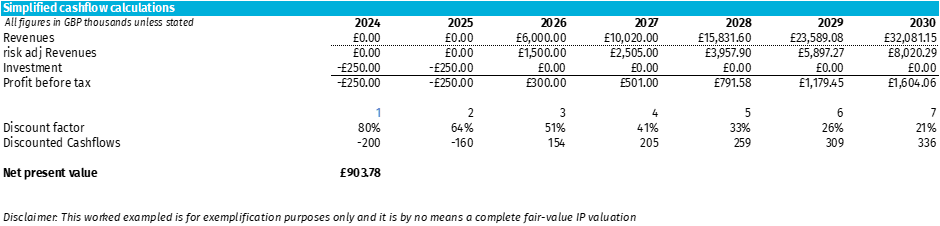

Lastly, by analysing the market and the competitors in the UK, we settle to price the product at £4,000, thanks to which we can now forecast the revenues for the first five years after the launch. To be able to use the discounted cashflow method, we can apply a percentage (in line with the industry – 20% for the purposes of this worked example) of the revenues to be the profit before tax. At this stage, we can now forecast the cashflows for the first five years of commercialisation.

Disclaimer: profit before tax is not exactly cashflow, but it is used as a proxy for exemplification purposes.

However, in order to calculate the net present value of the technology, we would need a discount rate to account for the time value of money. £100 today is worth more than £100 in one year due to inflation and the opportunity cost of the investment’s money-making potential. In our current crazy inflationary environment, £100 today will be worth at most £91.74 in one year, assuming a 9% inflation rate.

There are many formal ways of assessing the discount rate, but there are also certain ballpark figures we can refer to. The current state of the economy has a significant impact on them, but as an indication, we can assume 10-25% for established businesses, 20-35% for scaling businesses, 30-40% for companies reaching product market fit, and 35% all the way to 80% for early-stage startup companies. Risk is also usually accounted for in the discount rate. The higher the risk, the higher the discount rate. The downside of using a large discount rate is that it is almost disregarding later forecasted years.

A way around using a very large discount rate of 70-80% is to add another factor to the mix to account for the risk separately. This success factor considers all the risks associated with the technology realising the forecasted revenues. The success factor can be further decomposed into technical, legal, commercial, regulatory, scaleup risks. Assigning a percentage between 1 to 100% for each category and then multiplying them will give you an overall success factor that can be applied to your revenues, which will lower the cashflows. After the application of the success factor, we are now ready to do the final calculations.

We have created a simple modelling tool which can be used by stakeholders involved in early-stage technology development in order to gain an indication of the ballpark value of their technology. Having obtained all the individual sets of data, we can now complete our valuation exercise. Thanks to the interactive tool, we can input the data and see what value we get for our fictive example – see figures 1 and 2.

Disclaimer: Many steps have been simplified for the purpose of this exemplification. A comprehensive valuation of technologies involves taking into consideration many other factors not accounted here.

If you want to try out the interactive valuation tool yourself, click here.

Whilst it is not easy to carry out an IP valuation of an early-stage technology, it allows investors, universities, and companies to understand the key factors affecting the value of their IP. Also, it leads to a more informed decision making regarding which technology to invest in at the expense of another. Mathys & Squire Consulting has significant experience in valuing deep tech early-stage technologies in various technical fields. Please get in touch with any IP valuation inquiries you might have.